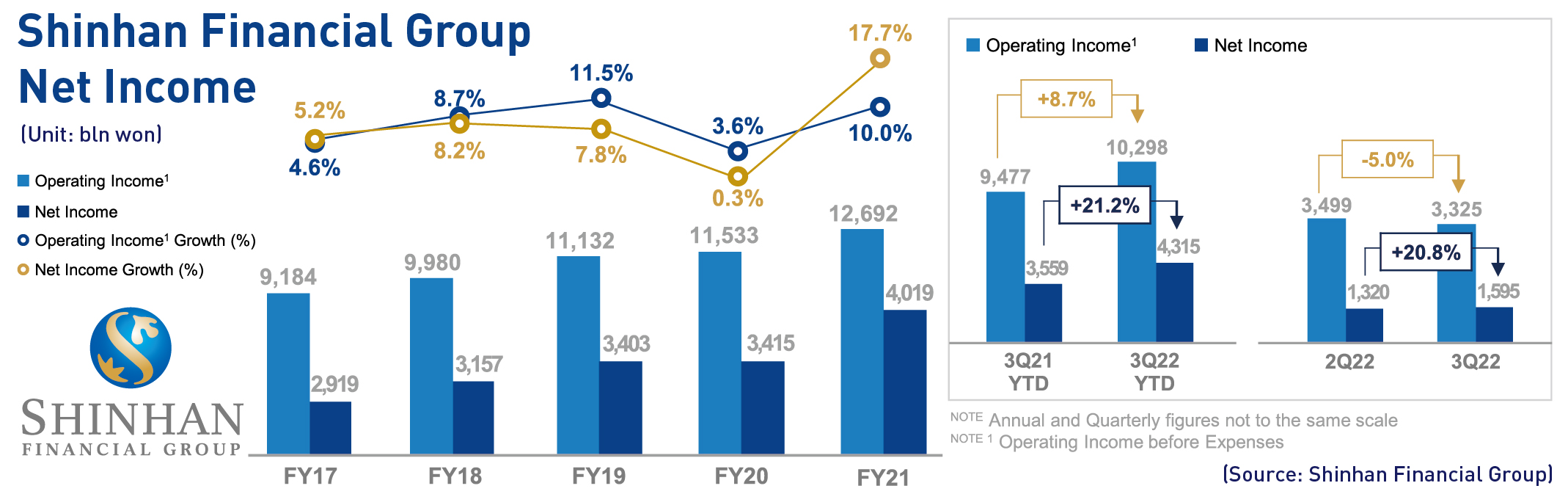

Shinhan Financial Group posted a record-high performance through the third quarter of this year thanks to an increase in interest income caused by a rise in the interest rate and proceeds from the sale of non-operating assets, such as Shinhan Securities Building.

Shinhan Financial Group announced on Oct. 25 that its cumulative net profit for the first three quarters of this year stood at 4,315.4 billion won, up 21.1 percent from the same period of 2021.

As of the third quarter, it posted a net profit of 1,549.6 billion won, an increase of 20.8 percent from the same period of the previous year.

Although non-interest income plummeted, led by that of Shinhan Securities, due to increased market volatility, such as the interest rate and exchange rates, its earnings improved.

Shinhan Bank’s net interest margin (NIM) rose, and loan assets continuously grew centered on corporate loans.

Shinhan Financial Group’s third quarter interest income stood at 2,716.0 billion won, up 2.7 percent from the previous quarter. Cumulatively, the figure amounted to 7,847.7 billion, an increase of 17.8 percent compared to the same period of 2021.

Shinhan Financial Group’s and Shinhan Bank’s third-quarter NIMs were 2 percent and 1.68 percent, respectively, improving 2bp and 5bp quarter on quarter.

The bank’s NIM rose by 5bp thanks to an improvement in its loan asset yield following a rise in the benchmark interest rate.

But an improvement in the group’s NIM compared to the bank’s NIM shrank due to an increase in credit card financing costs.

Shinhan Financial Group’s cumulative NIM in the third quarter improved to 1.96 percent while Shinhan Bank posted an NIM of 1.61 percent during the same period.

But the rate of their increases gradually slowed down as a funding interest rate rose in earnest.

The financial group‘s interest income in the third quarter sat at 609.2 billion won which represented an increase of 28.8 percent from the previous quarter due to a decrease in both commission income and securities-related gains.

Its commission income contracted 16.1 percent quarter on quarter due to a decrease in commissions for credit card use, securities custody, and investment finance, while its securities-related gains fell 22.9 percent quarter on quarter due to valuation losses caused by a sharp rise in the interest rate.

Its cumulative non-interest income in the third quarter was only 2,450.8 billion won, down 12.9 percent from the same period of 2021 as its commission income stayed at the level of the same period of 2021.

But its securities-related income descended by 18.7 percent compared to the same period of the previous year.

In the third quarter, its loan loss expenses shrank by 30.0 percent from the previous quarter to 250.6 billion won due to the base effects of 224.5 billion won in additional provisions accumulated in the second quarter.

Its accumulated bad debt expenses in the third quarter stood at 852.4 billion won, up 50.8 percent or 287.1 billion won from the same period of the previous year due to the effects of additional provisions accumulated in the first half of 2022.