The global semiconductor market is predicted to grow about 11 percent this year despite the effects of the reverse base effect of the best-ever business performance last year. The global semiconductor market saw a 24.6 percent jump last year.

Three survey institutions readjusted their earlier outlooks upward based on major companies’ good business performances in Q1 2022, and reported that the global semiconductor market is forecast to grow 11 percent in the whole of the semiconductor sector — a 14.9 percent surge in the memory segment and a 9.5 percent increase in the system semiconductor segment.

The survey institutions predicted the growth of the global memory market will range from about 1.1 percent to 28 percent, due to the expanded uncertainties, caused by global risks.

As the Philadelphia Index, a leading market outlook index, maintained a downward decline after the end of March and Korean semiconductor-related stock prices did not surge so far this year, market uncertainties remain.

Despite large growth in 2021, Q1 2022 business performances surpassed market consensus and the market for this year is expected to maintain a growth cycle.

The outlooks for memory prices for the second half of the year is hard to predict due to the expanded uncertainties of supply chains, caused by Shanghai’s lockdown and Russia’s invasion of Ukraine.

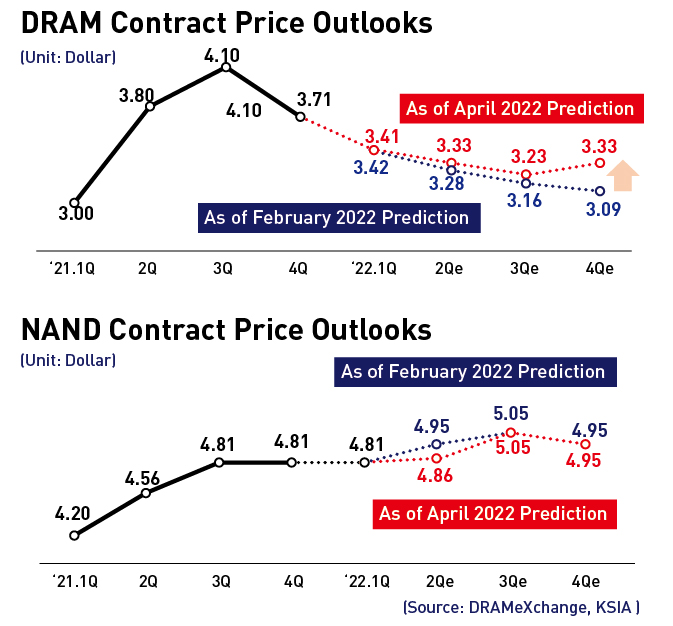

DRAM prices are expected to rise in the fourth quarter on the back of the expanded server demand and DDR5.

DRAM spot prices shifted to a decline in the 2022 Q1, contract prices maintained a steady trend before dropping a little margin. On the other hand, NAND flash memory prices continued to rise.

As for contract prices, DRAMS declined a little, and NAND flash memories have showed a steady tone since the second half of last year.

Memory prices cannot be predicted due to the expanded uncertainties of supply chains, but DRAM spot prices are expected to rise in the fourth quarter of the year.

If second-half demand improves following disruption of Kioxia’s production, NAND memory prices are forecast to decline in the second half.

Unstable macro situations, such as the protracted Russia-Ukraine conflict, China’s lockdown against the COVID-19 pandemic, interest rate hikes and high inflation fears, are expected to force companies to maintain a conservative investment mode, so lower-than-expected supply increase is predicted to stop a price drop and turn into a rise for the fourth quarter.

Prices of SSDs for companies remained steady on the back of the demand of data centers, but fears of declining demand of consumer IT gadgets in the second half and rising production by new suppliers are forecast to worsen a supply glut, so NAND flash memory prices are expected to plunge more than 5 percent.

Demand is expected to slow down compared to a high growth in 2021, but demand still remains steady. The server sector with a higher portion is predicted to continue a steady shipment, but mobile, PC, and notebook shipments are forecast to decline compared to the previous year.

Major companies did not release new CPUs and implement investments due to the COVID-19 pandemic. On the back of their rising investment in the cloud segment, demand for server DRAMs is predicted to maintain a steady tone.

Smartphone demand is expected to be sagging due to the lockdown of Chinese cities, but demand is likely to improve on the back of Apple, Samsung Electronics and Chinese companies’ release of new products in the third quarter of the year.

Non-face-to-face demand, such as home work and remote learning, which led last year’s memory demand rise, is expected to decline, so PC demand is also showing signs of decline.

Overall supply is predicted to be restrictive due to declining memory demand and DRAM makers’ conservative investment trends. On the other hand, NAND flash memory segment is feared to face a supply glut in the second half due to some suppliers’ trends of expanding production capacities.

The foundry segment is forecast to continue to be in short supply in the second half. As TSMC and Samsung Electronics have raised prices, late-comers like GlobalFoundries and SMIC are expected to increase foundry chip prices.

The nation is predicted to see exports achieve the best-ever performance this year. Exports are forecast to stand at $140 billion in 2022, a 10.2 percent year-on-year jump.

The nation saw exports surge a 29 percent year-on-year jump to $128 billion, the best-ever achievement, last year.

The semiconductor supply and demand is expected to improve due to companies’ conservative investment trends, caused by interest rate hikes and Russia’s invasion into Ukraine. Exports are likely or rise on the back of the continued good business performance of the foundry business.

The memory segment is predicted to post between $87 billion and $88 billion in exports, about 6.2 percent year-on-year increase from $82.4 billion in 2021.

The nation saw exports maintain a steadier tone in 2022 Q1 than expected earlier. Demand for consumer IT gadgets were feared to decline in the wake of the lockdown of Chinese cities, but a steady demand such as servers are forecast to rise compared to the previous year.

The system semiconductor segment is predicted to export between $48 billion and $49 billion, an about 20.8 percent year-on-year jump on the back of the continued improving of foundry industry’s business performance, renewing the best-ever export record of exporting $39.8 billion last year.